What is an escrow account?

Think of it like a savings account dedicated to the tax and/or insurance expenses required for your property—and as your loan servicer, we help you manage it. Depending on the terms of your mortgage, your escrow account may be set up for property taxes, homeowner's/hazard insurance, flood insurance, and/or mortgage insurance. A portion of your monthly mortgage payment is deposited into your escrow account, and these funds are reserved to pay your tax and/or insurance bills when they are due.

How does escrow work?

Each month, we deposit a fixed portion of your mortgage payment into your escrow account to cover your expected tax and/or insurance expenses, plus a little extra money in case these expenses increase from year to year—this is known as a cushion. Then, we pay each bill out of your escrow account on your behalf.

Since tax and insurance bills can change from year to year, we review your escrow account at least annually to make sure your balance is sufficient. Then, we send you an Escrow Account Disclosure Statement to inform you of any changes in your escrow activity, as well as any corresponding changes to your monthly payment.

What are the advantages of having an escrow account?

Having an escrow account can save you time and make homeownership easier. Escrow helps you budget for large expenses required for your property, giving you peace of mind. We fully manage the account for you, paying your tax and/or insurance bills on your behalf when they are due. We also review your escrow activity at least annually to help ensure the balance is sufficient based on your expected expenses.

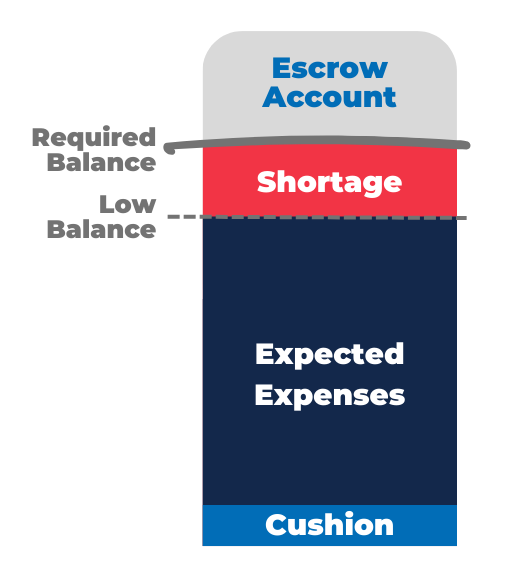

What is an escrow shortage?

What is an escrow shortage?

What is an escrow shortage?

What is an escrow shortage?All escrow accounts have a minimum required balance, which equals your expected tax and insurance expenses plus some extra money in case your bills go up – this is called a cushion. If your escrow account balance is expected to dip below the minimum required balance in the upcoming 12 months, you have a shortage. In other words, your escrow account will not have enough funds for the upcoming year unless you increase the balance.

How did I end up with a shortage?

Reasons you do not have enough money in your escrow account to meet the minimum balance may include:

- Increase in the rate of your insurance premium.

- Your property value was reassessed, leading to a change in property taxes due.

- Change in your insurance provider or policy.

- Change in the due date of your property taxes and/or insurance premiums.

- Your payments into your escrow account were fewer or less than expected.

- Starting escrow balance for the upcoming year is lower than expected due to higher expenses in the prior year.

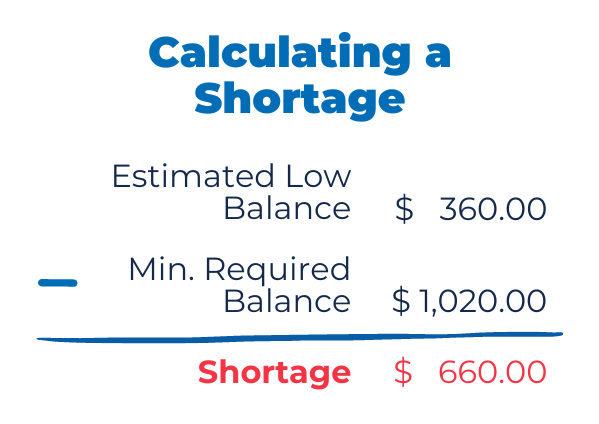

How is a shortage calculated?

How is a shortage calculated?

How is a shortage calculated?

How is a shortage calculated? The difference between the low balance and the required balance shows the amount of your escrow shortage. For example, see the calculation on the right with sample data. If your Escrow Account Disclosure Statement shows a shortage, the section titled Expected activity in the upcoming year shows exactly how we calculated it.

What do I need to do?

It is necessary to repay the shortage to help ensure your escrow account satisfies the minimum required balance.

Some good news: You don’t have to repay a shortage immediately or all at once. A shortage is automatically spread across your upcoming mortgage payments, typically for 12 months. The first page of your escrow statement provides the date on which you need to begin making your mortgage payments in the new amount.

If you want to minimize the increase in your monthly payment, you can choose to make a lump sum payment at any time to reduce or fully repay the shortage. This is not required; we offer the option for those who want to keep their monthly mortgage payment as low as possible. If you choose to pay down your shortage, the new monthly mortgage payment provided on the first page of your escrow statement will be reduced.

How can I make a lump sum shortage repayment?

If you opt to repay some or all of your shortage, you can choose from the following payment options:

- Online: Log into your account via our website or app, go to Payment, select other payment types, and enter your chosen amount into the additional escrow field.

- By Phone: Call Customer Care.

- By mail: Send a check to our Payments address. Be sure to write “escrow shortage repayment” and your loan number on the check.

If I repay my shortage in full now, will my monthly payment still increase?

Repaying your shortage in full will not prevent your monthly payment from increasing. If your tax and/or insurance expenses have increased, it is necessary to increase your monthly payment amount to cover your upcoming bills.

At least once per year, we are required to update the amount of your monthly payment every 12 months based on the amount of your tax and/or insurance expenses in the prior 12 months. If your expenses change, the amount you pay into your escrow account each month as part of your monthly mortgage payment needs to be adjusted accordingly. This can help prevent or lessen a shortage next time your escrow account is reviewed.

What do I need to do if my payment changes?

It is important to note your new monthly mortgage payment amount and effective date provided in your escrow statement and to adjust your payment accordingly.

If your monthly mortgage payment is set up for automatic payments (monthly or biweekly ACH drafts) through us, your draft settings will automatically update with the new amount of your monthly mortgage payment on the effective date. If you make your mortgage payments through a third-party entity (e.g. bank, government allotment, biweekly, or bill-pay service), be sure to update your payment settings to the new amount.

Can I prevent a shortage from occurring in the future?

Since tax and insurance expenses can change without advance notice, shortages are not always preventable. However, keeping track of your escrow account activity can help you minimize a shortage in the future. If a tax or insurance bill paid out of your escrow account increases from the prior year, you could opt to pay the difference into your escrow account at that time. This will help ensure your escrow balance meets the requirement.

If you have provided us with your email address and have not opted out of receiving emails from us, we will send you an email each time a tax and/or insurance bill is paid on your behalf. You can also log into our website or app to review your escrow activity anytime.

I am concerned about repaying the shortage and/or the new monthly mortgage payment. What should I do?

If you anticipate these changes could lead to financial hardship, we want to help. Please reach out to our Homeowner Assistance Team. We will guide you on mortgage assistance options available, how to apply, and what to expect.

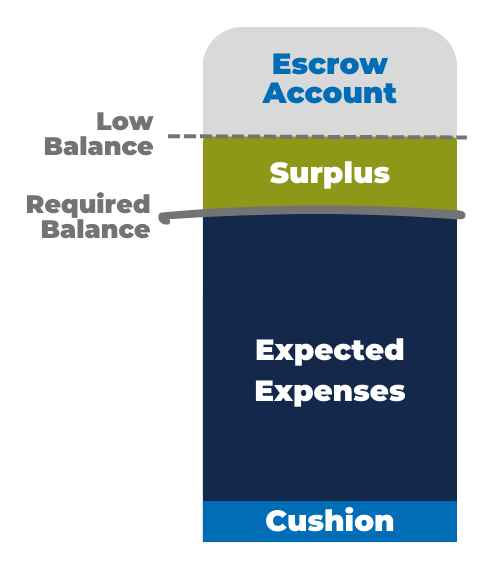

What is an escrow surplus?

What is an escrow surplus?

What is an escrow surplus?

What is an escrow surplus? All escrow accounts have a minimum required balance, which equals your expected tax and insurance expenses plus some extra money in case your bills go up – this is called a cushion. If your escrow account balance is more than the minimum required balance, you have a surplus.

How did I end up with a surplus?

Your escrow account contains more funds than needed to cover your expected escrow expenses in the upcoming 12 months. This may be due to a decrease in your taxes and/or insurance expenses, or because you paid more money into your account than expected last year.

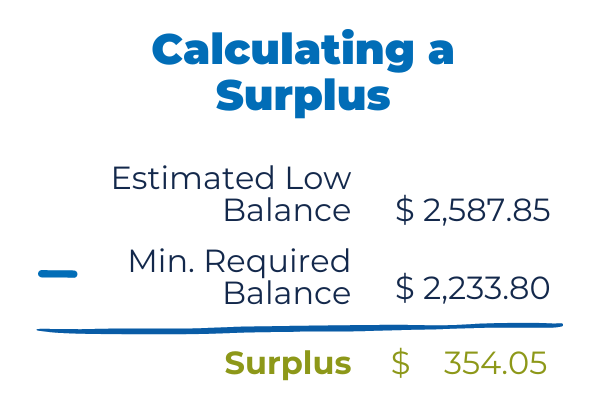

How is a surplus calculated?

How is a surplus calculated?

How is a surplus calculated?

How is a surplus calculated? Subtracting the expected minimum required balance from the estimated low balance shows the amount of your escrow account surplus. For example, see the calculation on the right with sample data. If your Escrow Account Disclosure Statement shows a surplus, the section titled Expected activity in the upcoming year shows exactly how we calculated it.

What happens to the extra money?

If your escrow surplus is less than $50, a credit in the amount of your surplus will be automatically spread across your upcoming monthly mortgage payments.

If your escrow surplus is $50 or more, the amount of the surplus will be refunded to you.

A surplus of any amount may be retained if mortgage payments are past due or if the mortgage is in default or bankruptcy.

I have a surplus, but my monthly mortgage payment went up. Why?

Even if you have a surplus, we are required to update the amount of your monthly escrow payment every 12 months based on the amount of your tax and/or insurance expenses in the prior 12 months. If your expenses have changed, the amount you pay into your escrow account each month as part of your monthly mortgage payment must be adjusted accordingly.

I am concerned about the new amount due for my monthly mortgage payment. What should I do?

If you anticipate these changes could lead to financial hardship, we want to help you navigate mortgage assistance options available for your loan. Please reach out to our Homeowner Assistance Team.

Why did my payment change?

When your taxes and/or insurance bills change from year to year, it may be necessary to adjust the amount you are paying into your escrow account, too.

Reasons your expenses changed may include:

- Insurance: Changes to type, extent, due date, rate, insurance policy, or carrier.

- Real estate taxes: Property value, tax rate, or due date changed.

- Your property value changed: If you have built a new home or renovated it, your property value will likely increase. Any substantial improvement to your property will likely increase your property taxes.

- Initial escrow deposit: Escrow costs may be estimated at loan closing if the information is unavailable. If the amount collected to set up your escrow account was more or less than your actual costs, your payment will be adjusted accordingly.

- Shortage: Your balance is expected to fall below your Minimum Required Balance. A shortage repayment is automatically divided across your payments for the upcoming 12 months, increasing your monthly payment. See our Escrow Shortage FAQs for more information.

I have a surplus, but my monthly mortgage payment went up. Why?

Even if you have a surplus, we are required to update the amount of your monthly escrow payment every 12 months based on the amount of your tax and/or insurance expenses in the prior 12 months. If your expenses have changed, the amount you pay into your escrow account each month as part of your monthly mortgage payment must be adjusted accordingly.

I am concerned about the new amount due for my monthly mortgage payment. What should I do?

If you anticipate these changes could lead to financial hardship, we want to help. Please reach out to our Homeowner Assistance Team. We will guide you on mortgage assistance options available for your loan and how to apply.

What do I need to do if my payment changes?

It is important to note your new monthly mortgage payment amount and effective date provided in your escrow statement. Remember to adjust your payment amount accordingly beginning on the effective date.

If your monthly mortgage payment is set up for automatic payments (monthly or biweekly ACH drafts) through us, your draft settings will automatically update with the new amount of your monthly mortgage payment on the effective date.

If you make your mortgage payments through a third-party entity (e.g. bank, government allotment, biweekly, or bill-pay service), be sure to update your payment settings to the new amount.

I am concerned about the new amount due for my monthly mortgage payment. What can I do?

If you anticipate these changes could lead to financial hardship, we want to help. Please reach out to our Homeowner Assistance Team. We will guide you on mortgage assistance options available, how to apply, and what to expect.

How can I see my escrow account activity?

As your mortgage partner, we strive to make it easy to view and understand your escrow activity. We provide 24/7 access to track your escrow balance, deposits, and disbursements online, plus other easy ways to stay informed of your escrow account activity.

Email notifications: If you have provided your email address and have not opted out of receiving emails from us, we will send you an email each time we pay a tax and/or insurance bill from your escrow account on your behalf.

Monthly mortgage statement: The amount deposited into your escrow account from your mortgage payment each month, as well as any tax and/or insurance bills paid out of your escrow account, will appear under Transaction Activity.

Online: You can access your escrow account information 24/7 on our website or mobile app in the My Loan section.

In addition, any time you have questions, our Customer Care team will be happy to help. You can send us a secured message anytime from your online account, or reach out to us by phone or email. We are eager to serve you!